Life insurance for married couples is crucial. It provides financial security and peace of mind.

When you get married, your financial future becomes a shared journey. It’s important to protect that future. That’s where life insurance comes in. It’s a smart move. It makes sure your partner is taken care of if something unexpected happens.

This kind of security helps cover:

- Everyday expenses

- Debts

- Future plans

So, why is life insurance a big deal for married couples? Let’s break it down. This guide will walk you through the basics. You’ll learn why it’s important and how it can help you and your partner feel secure about your future together.

Credit: www.bankrate.com

Importance Of Life Insurance

Hey there! Let’s talk about something really important for married couples: life insurance. It’s all about making sure your family is okay financially, even if something happens to one of you. Here’s why having life insurance matters:

Financial Security

Life insurance gives your spouse and kids financial security. The money from the policy can help with:

Mortgage payments

Daily living costs

School fees for the kids

Any outstanding debts

This money helps your family keep up their lifestyle and cover what they need. Without it, they might have a hard time getting by.

Peace Of Mind

Having life insurance brings peace of mind. You know your loved ones are taken care of. This can really lower stress and anxiety. You can live your life knowing there’s a safety net in place. It’s a comforting thought for any married couple

| Benefit | Explanation |

|---|---|

| Financial Security | Ensures your family can maintain their lifestyle. |

| Debt Coverage | Prevents your family from inheriting your debts. |

| Peace of Mind | Reduces stress knowing your family is protected. |

Types Of Life Insurance

As a married couple, selecting the right life insurance policy is vital. Understanding the different types of life insurance can help you make the best choice. Let’s dive into the two main types: Term Life Insurance and Whole Life Insurance.

Term Life Insurance

Let’s talk about Term Life Insurance. It’s a favorite among married couples for a reason. It covers you for a set period, usually between 10 and 30 years. If something happens to you during this time, your loved ones get a payout.

Why Choose Term Life Insurance?

- Affordable Premiums: Costs less than many other types.

- Fixed Term: Coverage lasts for a specific number of years.

- Simple to Understand: Easy to grasp without a lot of jargon.

Term Life Insurance is perfect if you need coverage for a particular time. Think about it like this: It can help with mortgage payments or your kids’ college costs.

Now, let’s dive into Whole Life Insurance. Unlike Term Life, it doesn’t expire. As long as you keep up with payments, you’re covered for life. Life Insurance for Married Couples

Key Features of Whole Life Insurance

- Lifetime Coverage: Stays valid as long as you pay the premiums.

- Cash Value: Builds up cash you can borrow against.

- Fixed Premiums: Your payments stay the same throughout the policy.

Whole Life Insurance is great if you want long-term security. Plus, it can act like an investment because of the cash value it builds.

So, how do you choose between Term and Whole Life Insurance? Think about your financial situation and what you need in the long run. Each has its own perks to help protect your family’s future.

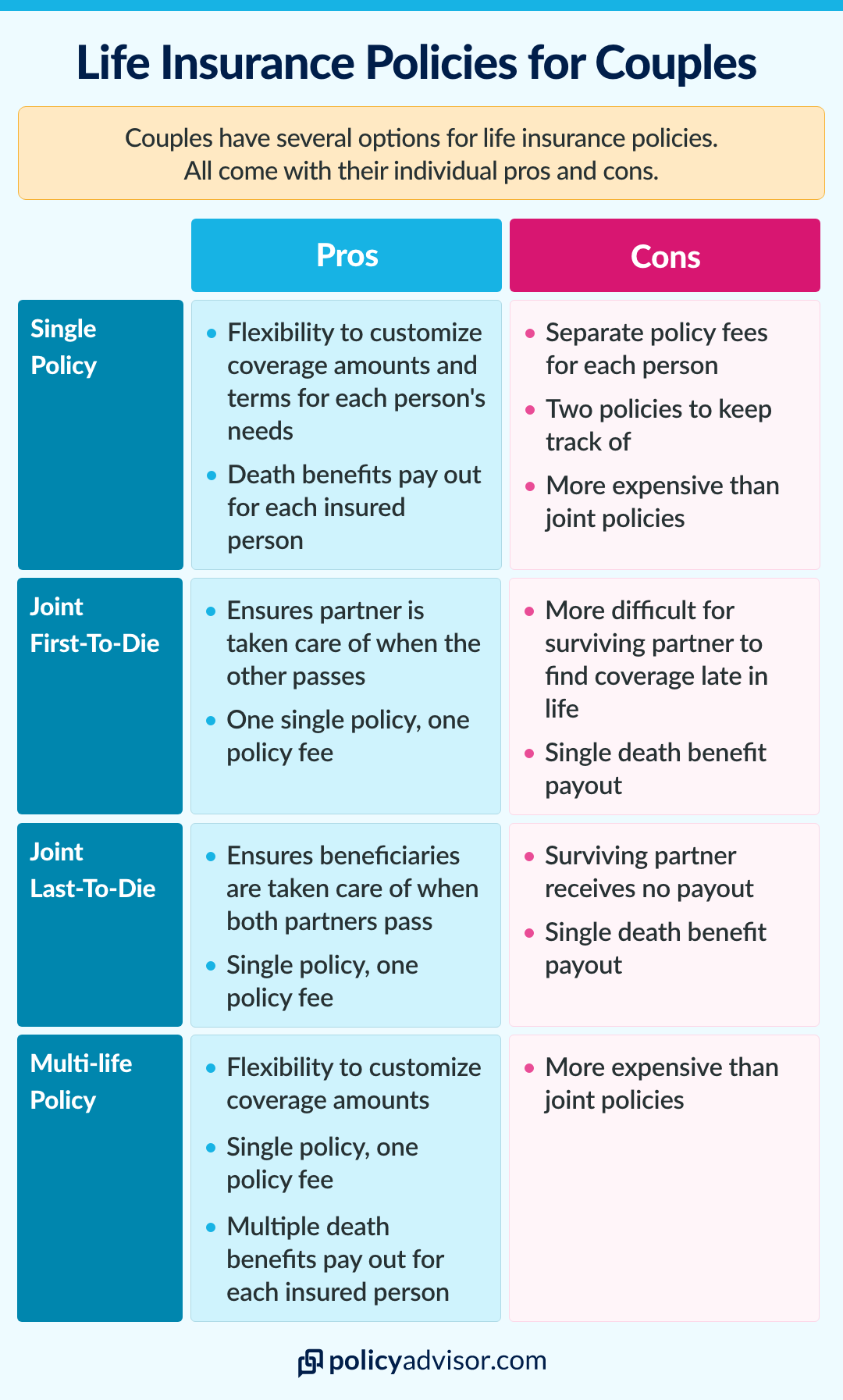

Joint Life Insurance Policies

Life insurance is something every married couple should think about. It gives financial security if something unexpected happens. One good option is a joint life insurance policy. This covers both partners under one plan.

There are two common types of joint life insurance policies:

First-to-Die Policy

This policy pays out when the first partner dies. It provides quick financial help for the surviving partner. Think of it as a safety net. It can cover things like:

- Living expenses

- Outstanding debts

- Funeral costs

Only one payout is made, and the policy ends after the first death. It can be cheaper than buying two separate policies. This is a good choice for couples who depend on each other’s income.

Second-to-Die Policy

This policy is different. It pays out after both partners have passed away. It’s often used for estate planning and leaving a legacy for children. Also called a survivorship policy, it can help with:

- Estate taxes

- Leaving an inheritance

The payout happens only after both partners die. It can also be more affordable than two separate policies. This is ideal for couples who want to ensure their kids or beneficiaries are well taken care of.

The bottom line? Picking the right joint life insurance policy depends on what you need and your goals. Knowing your options can help you make the best choice.

Life Insurance for Married Couples

Choosing The Right Coverage Amount

Choosing the right coverage amount for life insurance is crucial for married couples. It ensures financial stability and peace of mind. The correct coverage can help protect your loved ones from financial hardships in your absence. Here are key factors to consider.

Income Replacement

One major reason for life insurance is income replacement. If one spouse passes away, the other may face financial challenges. Replacing lost income helps maintain the same living standards. Calculate the total annual income that would be lost. Then, consider how many years the income needs to be replaced.

| Annual Income | Years to Replace | Total Coverage Needed |

|---|---|---|

| $50,000 | 10 | $500,000 |

| $75,000 | 15 | $1,125,000 |

Debt Coverage

Married couples often have shared debts. These can include mortgage, car loans, and credit card debt. Life insurance can help cover these debts. Calculate the total outstanding debt. This ensures your spouse doesn’t struggle to pay off these debts alone.

- Mortgage: Calculate the remaining balance on your mortgage.

- Car Loans: Add up any remaining car loan balances.

- Credit Card Debt: Include any outstanding credit card balances.

Adding these amounts gives you the total debt coverage needed. For example:

| Debt Type | Remaining Balance |

|---|---|

| Mortgage | $200,000 |

| Car Loan | $15,000 |

| Credit Card | $5,000 |

Total debt coverage needed: $220,000.

By assessing both income replacement and debt coverage, you can determine the right life insurance coverage for your needs.

Beneficiary Designations

Beneficiary designations are crucial in a life insurance policy. They determine who receives the death benefit after the insured passes away. For married couples, it is essential to understand the types of beneficiaries.

Life Insurance for Married Couples.

Primary Beneficiary

The primary beneficiary is the first in line to receive the death benefit. Most married couples choose their spouse as the primary beneficiary. This ensures financial security for the surviving partner. It is important to name a specific person. Avoid general terms like “spouse” or “children.” This prevents confusion and legal issues. Always update the primary beneficiary if circumstances change, like a divorce or new child. Life Insurance for Married Couples

Contingent Beneficiary

The contingent beneficiary receives the death benefit if the primary beneficiary is deceased. This designation is a backup plan. It ensures the policy benefits go to the intended person. Many couples choose their children or a trusted relative as contingent beneficiaries. This step provides an extra layer of security. Like the primary beneficiary, name specific individuals. Avoid using vague terms. Regularly review and update the contingent beneficiary. Life changes, so should your policy designations.

Credit: www.policyadvisor.com

Policy Riders And Add-ons

Life insurance for married couples often includes policy riders and add-ons. These provide extra benefits and flexibility. They can be customized to meet unique needs. Below, we explore some common riders and add-ons. Life Insurance for Married Couples

Waiver Of Premium

The Waiver of Premium rider is a valuable add-on. It ensures your policy stays active if you become disabled. You won’t have to pay premiums during disability. This rider offers peace of mind. It ensures your family remains protected.

Accidental Death Benefit

The Accidental Death Benefit rider provides extra coverage. It pays out an additional amount if death occurs due to an accident. This rider can double or triple the benefit. It offers extra financial support. This can be crucial in unexpected situations.

Cost Considerations

Understanding the costs of life insurance is crucial for married couples. Different policies come with different expenses. Knowing these costs helps in making an informed decision. This section covers the primary cost considerations, starting with premiums and policy fees.

Premiums

Premiums are the regular payments made to keep the insurance active. These can be monthly, quarterly, or annually. The amount varies based on age, health, and the type of policy. Term life insurance premiums are usually lower than whole life insurance premiums. It’s essential to compare different plans. This ensures you get the best value for your money.

Policy Fees

Policy fees are additional charges that come with life insurance. These fees can include administrative costs and other service charges. Some policies have higher fees due to added benefits. It’s important to read the fine print. Understanding these fees avoids surprises later on. Always ask your insurance provider for a detailed breakdown of all costs.

Regular Policy Reviews

Life insurance policies are not set in stone. For married couples, regular reviews are crucial. These check-ins ensure the policy meets current needs. Life changes and financial updates often require adjustments. Reviewing your policy keeps you protected. Let’s delve into why these reviews are necessary. Life Insurance for Married Couples

Life Changes

Life never stands still. For married couples, this means constant changes. New children, new homes, or even new jobs. Each change impacts your life insurance needs. A regular review helps adjust the policy. This ensures it still provides the right coverage.

- New Family Members: Adding a child increases financial responsibilities.

- New Jobs: A new job may come with different benefits.

- New Homes: A larger mortgage requires more coverage.

Financial Updates

Financial situations change too. Maybe you paid off debt. Or your income increased. Each financial update affects your insurance needs. A regular policy review considers these changes.

| Financial Change | Impact on Policy |

|---|---|

| Paying Off Debt | May reduce the need for high coverage. |

| Increased Income | May allow for higher premium options. |

| New Investments | May need different types of coverage. |

Regular policy reviews ensure your life insurance remains relevant. They align with your current life stage and financial status. This keeps you and your loved ones secure.

Credit: www.ethos.com

Frequently Asked Questions

What Is Life Insurance For Married Couples?

Life insurance for married couples provides financial security for your spouse in case of your death. It ensures your partner can cover expenses like mortgage, debts, and daily living costs.

Why Should Married Couples Get Life Insurance?

Married couples should get life insurance to protect each other financially. It offers peace of mind, knowing your spouse will be taken care of if something happens to you.

How Much Life Insurance Should Couples Have?

Couples should consider their financial obligations and future expenses. Calculate your debts, mortgage, and living costs to determine the right coverage amount.

What Are The Benefits Of Joint Life Insurance?

Joint life insurance policies are often cheaper than two individual policies. They offer coverage for both spouses under one policy, which can simplify management. Life Insurance for Married Couples

Conclusion

Life insurance is crucial for married couples. It provides financial security. Protect your family’s future with the right policy. Discuss options with your spouse. Evaluate your needs together. Choose a plan that fits your budget. Peace of mind is invaluable.

Life insurance can offer that. Research different providers. Compare their offerings and prices. Make an informed decision. Your loved ones will appreciate it. Stay prepared for whatever life brings. Start planning today.